Trouvez vos futurs bureaux

à Paris et en Île-de-France

Nos services

Knight Frank est un conseil international en immobilier. Spécialiste en immobilier tertiaire et résidentiel, Knight Frank bénéficie d’un positionnement unique dans le monde du conseil immobilier.

Bureaux

Knight Frank conseille et accompagne les entreprises dans la commercialisation de leurs actifs.

En savoir plus Bureaux

Investissement

Conseil et accompagnement en investissement en immobilier commercial en France.

En savoir plus Investissement

Commerces

Location et vente de boutiques à Paris et en France pour le compte de clients français et internationaux.

En savoir plus Commerces

Concevoir et aménager vos bureaux

Knight Frank Design & Delivery accompagne les entreprises dans leur aménagement d'espaces.

En savoir plus Travaux et Aménagements

Expertise

Knight Frank Valuation & Advisory une gamme complète de services d'expertise immobilière.

En savoir plus ExpertiseNos offres immobilières

Coworking

Consulter nos offres

Bureaux

Consulter nos offresNos références

-

Bureaux

MADE IN

Saint-Ouen

2 494 m²

-

Bureaux

Maslö

Levallois-Perret

2 262 m²

-

Bureaux

53 boulevard Haussmann

Paris, 9ème

1 843 m²

-

Bureaux

22 rue Bergère

Paris, 9ème

2 882 m²

-

Bureaux

WING

Boulogne-Billancourt

2 672 m²

-

Bureaux

CAPITAL 8

Paris, 8ème

1 829 m² - 3 200 m²

-

Bureaux

10 rue de Bassano

Paris, 16ème

1 747 m²

-

Bureaux

64 Rue de Lisbonne

Paris, 8ème

7 882 m²

-

Bureaux

41-43 rue Saint-Dominique

Paris, 7ème

2 555 m²

-

Commerce

Dior

Immobilière Dassault / Dior

Paris 08

2 500 m²

-

Commerce

IKEA

Invesco / IKEA

Paris 01

2 900 m²

-

Commerce

Kith

Meyer Bergman / KITH

Paris 08

1 500 m²

-

Investissement

Portefeuille Bricks

Unibail Rodamco Westfield / Primonial

Calais - Roubaix

33 000 m²

-

Investissement

Portefeuille Leonardo

Blackstone / UBS

Paris 08

1 800 m²

-

Investissement

Le Printemps

LaSalle Investment Management / Unofi

Lille

24 700 m²

-

Investissement

Place des Halles

Hammerson / AEW / LaSalle IM

Strasbourg

46 000 m²

-

Investissement

Carré Saint Germain

AXA IM / Tishman Speyer

Paris 06

13 000 m²

-

Investissement

Renaissance

Lagardère / Ardian

Paris 08

10 000 m²

-

Investissement

M Campus

AXA IM – NBIM / PGIM

Meudon

45 000 m²

-

Investissement

Cap Ampère

AEW / Ivanhoé Cambridge

Saint-Denis

90 000 m²

-

Investissement

Vivacity

Blackstone / Amundi

Paris 12

24 500 m²

-

Investissement

Logements intermédiaires

France entière

97 500 m²

-

Investissement

Portefeuille de locaux d’activités

3 sites en Île-de-France

4.500 m²

-

Investissement

Portefeuille d’actifs logistiques

4 sites en France

173.500 m²

-

Investissement

Portefeuille de bureaux

Paris

11 actifs

-

Investissement

Bureaux Paris Ouest

Banlieue Ouest de Paris

17.600 m²

-

Bureaux

23-25 rue de l’Université

Paris, 7ème

3 971 m²

-

Bureaux

Freedom

Paris, 16ème

16 000 m²

-

Bureaux

5-9 rue Van Gogh

Paris, 12ème

8 000 m²

-

Bureaux

173 boulevard Haussmann

Paris, 8ème

11 000 m²

-

Bureaux

Sways

Issy-les-Moulineaux

40 000 m²

Ils nous ont fait confiance

Notre actualité, nos engagements

Nos publications

Knight Frank conseille et accompagne les entreprises dans la commercialisation de leurs actifs.

En savoir plus

Nos partenaires

Knight Frank étend son réseau mondial et éuropéen avec deux nouveaux partenaires.

En savoir plusNotre présence

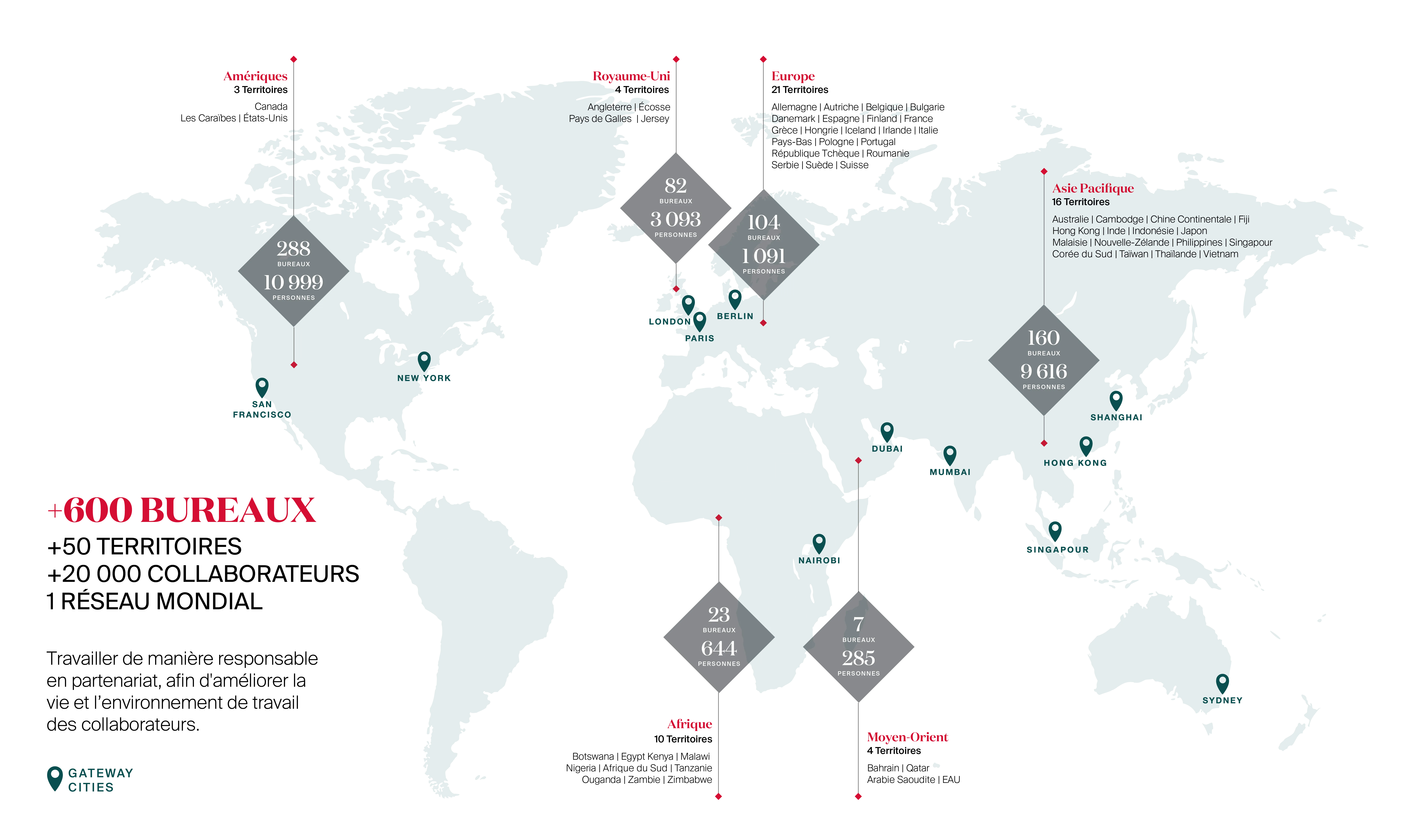

Fondé il y a 125 ans en Grande-Bretagne, le groupe Knight Frank

apporte aujourd’hui son expertise comme conseil international en immobilier.

0

territoires

0

collaborateurs

0

bureaux

Amériques 3 territoires

Royaume-Uni 3 territoires

Europe 18 territoires

Moyen-Orient 3 territoires

Asie Pacifique 15 territoires

Afrique 9 territoires

Guillaume Raquillet

Appeler Guillaume

Nous contacter

Indiquez-nous vos coordonnées et nous vous contacterons dans les plus brefs délais.

Guillaume Raquillet

01 43 16 88 88

Planifier une visite ou un rendez-vous

Indiquez-nous vos horaires de disponibilité et nous vous contacterons pour organiser une visite ou pour planifier un rendez-vous.